HOME BUYING GUIDE: IMPROVE YOUR CREDIT SCORE

A strong credit score is crucial to securing the best mortgage terms and rates when buying a home.

Understanding what constitutes a good credit score, as well as ways to improve it, can help prospective homebuyers navigate the real estate market more effectively.

Improving your credit score is essential for securing favorable mortgage terms and rates when buying a home in Sacramento. Conventional loans typically require a minimum credit score, but understanding and improving your score can open up better loan options and make homeownership more affordable.

Learn about specific credit score requirements, budgeting, loan options, and strategies to improve and maintain your credit score for a successful home buying journey.

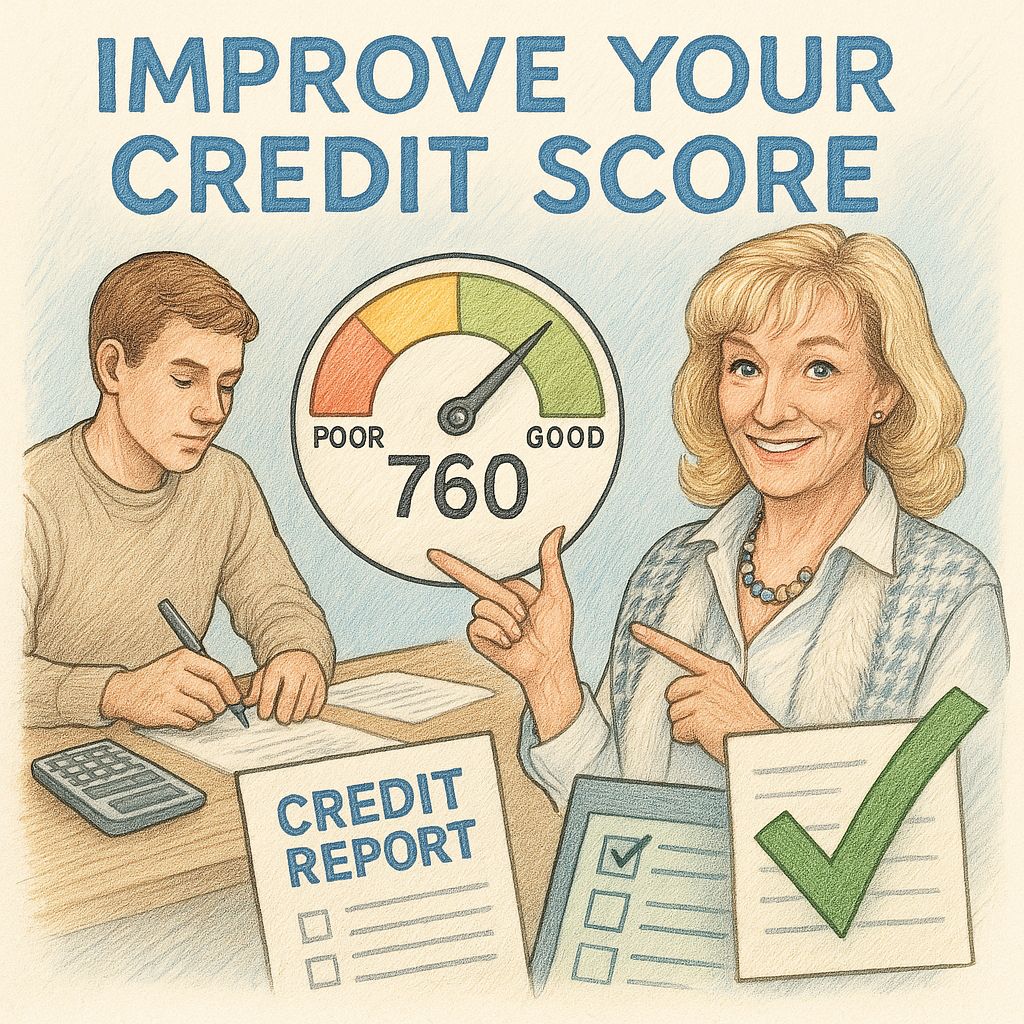

- 📈 Most conventional mortgages require a minimum score of 620 to secure good rates.

- 💵 FHA loans offer options starting at a credit score of 580, good for first-time buyers.

- 📝 Understanding your financial situation helps create a realistic home buying budget.

- 🔍 Check and correct errors in your credit report to improve your score.

- 💳 Keep credit utilization low—below 30% is ideal for a better score.

- ✅ Maintain regular on-time payments and manage existing debts effectively.

- 🏡 Explore loan assistance programs for down payment support and better rates.

In the Sacramento area, most conventional mortgage lenders typically require a minimum credit score of 620. However, higher scores can unlock better interest rates, ultimately reducing the overall cost of homeownership. Some loan programs, like FHA loans, allow for more lenient credit scores starting at 580, which can be beneficial for first-time buyers or those with blemished credit histories. It's essential to know the specific credit score thresholds for various loan types to plan your financial strategy accordingly.

Understanding the credit score requirements can significantly affect your mortgage rates—a higher credit score not only saves money but secures favorable loan terms, making the dream of homeownership more attainable.

Before jumping into the home buying process, it's vital to have a clear understanding of your financial situation. Prospective buyers should evaluate their income, debts, and savings to establish a realistic budget. Helpful tools like mortgage calculators can estimate monthly payments and determine overall affordability. Additionally, saving for a down payment and closing costs is crucial to avoid financial strain after purchasing a home.

A well-planned budget can provide peace of mind and help inform your decisions, ensuring you remain within your financial comfort zone while approaching homeownership.

Sacramento offers various loan options such as FHA, conventional, and VA loans to potential homebuyers. Each loan type has its own set of benefits and credit requirements. For first-time buyers or those with limited financial resources, programs like CalHFA provide down payment assistance and low-interest loans. Exploring eligibility for these assistance programs can significantly reduce the financial burden of buying a home.

Understanding and exploring different loan options ensures you are making an informed decision that aligns with your financial needs and long-term goals.

Improving your credit score is achievable through targeted strategies. Start by reviewing your credit reports for errors—these can negatively impact your score, and correcting them can lead to improvements. Focus on paying off existing debts and maintaining on-time payments to build a strong credit history. Keeping your credit utilization ratio below 30% can substantially enhance your score. Utilizing credit monitoring tools can help track progress and identify areas of improvement.

Implementing these strategies over time will enhance your credit score, laying the groundwork for better mortgage offers and other financial benefits.

Routine checks for errors in your credit report are pivotal. Mistakes can unjustly lower your credit score, hindering your home buying journey. Consumers can download free reports annually from the three major credit bureaus using annualcreditreport.com. The Fair Credit Reporting Act (FCRA) empowers consumers to dispute inaccuracies, so ensure timely corrections to boost your score.

By promptly identifying and resolving errors, you'll maintain a truer reflection of your creditworthiness, essential for mortgage approvals.

For a robust credit profile, avoid excessive new credit applications, manage existing debts effectively, and ensure regular on-time payments. Credit utilization should be kept low to maintain a positive score, and any major financial decisions should be made after securing a mortgage to avoid disrupting your credit profile during the loan process.

By nurturing a healthy credit profile, you’ll open doors to more financial opportunities and favorable mortgage conditions when you're ready to buy a home.